Population growth and high rates of urbanisation, coupled with climate change, have amplified financial and humanitarian losses incurred due to natural disasters over recent decades. While traditionally responding to need as it arose on the ground, the international community has recently re-oriented its approach towards the anticipation and mitigation of such events through risk assessment – a complex task for sporadic events such as hurricanes, earthquakes and floods.

Catastrophe models, traditionally developed in the private sector, have long been used by the insurance industry to help underwriters and investors understand, manage and price risks relating to extreme events. Such techniques are now beginning to be deployed by governments, NGOs and international aid agencies to assess and prepare for the risks posed by such disasters.

Over the past 25 years, the global population has risen by over a third from 5.3 billion in 1990 to over 7.1 billion in 2013,1 2 with much of that growth taking place in underdeveloped countries. While extreme weather events have always threatened the livelihoods of those in the poorest regions of the world, projected increases in the severity of such events due to climate change is further threatening those living in the most hazard-sensitive regions.

Traditionally, responding to natural disasters after the event has been the status quo. However, the concept of reducing the risk from disasters before they occur rather than dealing with the tragic consequences is moving ever higher on the list of global initiative priorities, driven by compelling evidence that every dollar spent on disaster risk reduction returns between 2 and 10 dollars in recovery savings.3 The latest World Development Report from the World Bank stated that “protecting hard-won development gains by building resilience to risk is essential to achieving prosperity. That is true whether one is grappling with natural disasters, pandemics, financial crises, a wave of crime at the community level, or the severe illness of a household’s chief provider”.4

Catastrophe modelling is essentially the process of quantifying the risk, damage and economic loss from natural hazards. Initially, this industry developed in the 1980s to assist property insurers and reinsurance companies to determine the risks to their financial portfolio from hurricanes in the United States. This was further driven by a number of large losses when Hurricane Hugo, the Loma Prieta Earthquake and Hurricane Andrew resulted in over $25 billion of loss between 1989 and 1992. The losses from Hurricane Andrew were particularly severe, rendering nine insurers insolvent.5 Accurate pricing of insurance premiums is essential for firms to be able to afford to compensate customers if disaster does strike. Meteorologists and engineers were recruited to provide underwriters with an estimate of the loss their insurance company could expect to cover on an annual basis. Research focussed on assessing the probabilities of tropical storms occurring and how they would interact with the built environment. In doing so, modelling companies contributed to a significant expansion of research into natural hazards and infrastructure vulnerabilities.

Although the complexity and scope of these models has grown extensively over the past 25 years there remain three key components driving their development: hazard, vulnerability and exposure (loss). This multi-disciplinary science involves meteorologists, hydrologists and seismologists, who work together to generate a set of simulated events which estimate the magnitude, location and probability of a natural hazard occurring. The damage caused by these events is then quantified by considering the vulnerability of different types of building to, for example, increasing wind speeds or degrees of shaking. Finally, this damage is aggregated over all exposed buildings and a loss estimate is derived.

The insurance industry has a long history of expertise and understanding in disaster risk management. However, predominantly driven by the marketplace the territorial scope of catastrophe models has, until now, been limited to countries where a significant percentage of the property exposure is insured. Those most in need of coverage are often uninsured, so their recovery is hampered by deep financial losses. Over time, the disproportionate impact of extreme events on the poorest societies most at risk from extreme events serves to further exacerbate pre-existing inequalities and development imbalances.

Same tools, different challenges

Changing the emphasis of disaster management towards risk reduction from loss estimation also means rethinking the typical modelling process. Just as with financial loss estimations, the key factors which need to be considered for disaster risk reduction are hazard, vulnerability and exposure. However, instead of considering what damage a particular hazard will cause, the focus shifts to asking what size event a particular community can withstand and how will this change if various structural mitigation measures are implemented, such as levees and flood walls. Policy-makers and disaster-response agencies can then combine this information with an awareness of the vulnerabilities of individual communities so that the potential social, economic and physical impacts can be anticipated.

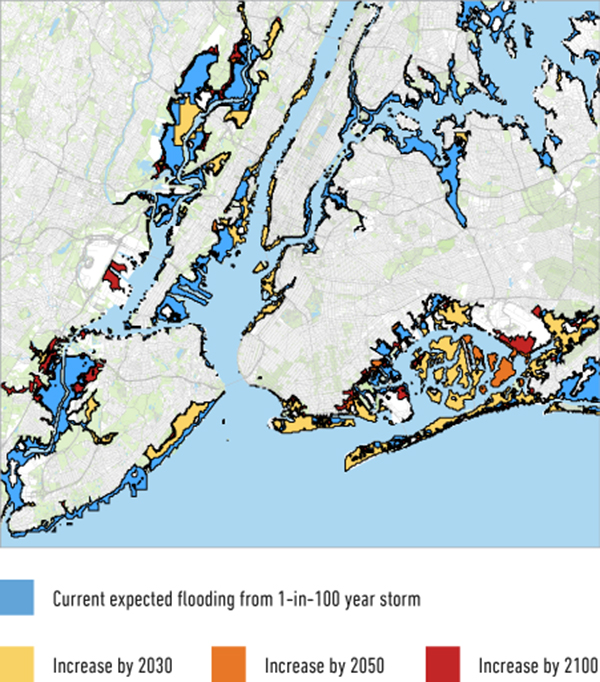

In regions which do not have a sufficient market driver to justify the development of a full model on financial grounds, the production of simple hazard maps may still be possible. These indicate, for example, the level of ground shaking corresponding to an event with an annual probability of 1% (1 in 100 years). Combining such hazard maps with population densities and data on building structures and average probabilities of collapse gives an indication of the likely number of casualties per year. Hazard maps can also be used to determine evacuation zones, and to estimate the number of people affected to assist emergency services in preparing for such an event. For example, if regional authorities have knowledge of the areas which are susceptible to flooding they can design evacuation routes and protocols which are optimised to the specifics of their local hazard.

This information is only useful, however, if properly understood in the context of the wider local issues and vulnerabilities. In particular, initiatives which address established behaviours and attitudes to risk in communities are a crucial part of a comprehensive disaster risk reduction programme. For example, if people are well informed, the development of early warning systems which enable evacuations for storm surges, tropical cyclones, tsunamis and floods can be more effective at saving lives and also more achievable than the step changes which are required improve the resilience of infrastructure in some of the countries most at risk. Earthquakes are an unfortunate exception to this; in regions with the most vulnerable buildings, reducing deaths from an earthquake is much more difficult due to the challenges of predicting seismic events on short timescales.

Isolated communities can particularly benefit from relatively simple educational measures which make use of coordinating efforts between scientific experts, engineers and local administrations. In Tajikistan, for example, project partners from all of these areas developed simple risk maps which used a clear colour-scheme to identify areas in local communities which were at risk from severe hazards and those which were much less likely to suffer. These risk maps were provided to individual village households in order to improve understanding of regions at risk from local rock fall and avalanches.6

Using science to drive policy

The ability to measure progress is an essential component of any evidence-based policy initiative. Reduction in the risks posed by natural hazards is difficult to quantify – what is an appropriate metric? Fortunately, catastrophic natural disasters are rare. However, this means that comparisons on short timescales of even a few decades are difficult. For example, in Haiti fewer than 10 people had been killed as a result of earthquakes between 1990 and 2009 but 220,000 died in one devastating event in 2010 and similarly nearly 300,000 people lost their lives due to the Boxing Day earthquake and tsunami in 2004.7 Thus, it is difficult to target a reduction in annual mortality or even economic loss due to disasters.

Again, this is where catastrophe modelling companies can play their part. Hazard maps indicating the likely human exposure to an extreme event provide metrics which can be combined across all countries and compared over time to evaluate global policies. As the number of low-lying communities which implement risk reduction measures increases, it becomes possible to quantify the reduction in the number of people at risk from a hazard, even if the likelihood and severity of the physical hazard itself does not change.

Despite the difficulty in discerning the exact impact of these disaster risk reduction measures, there is some evidence that active intervention has improved disaster mortality rates as well as reducing economic losses. For typhoons, the average annual mortality rate decreased rapidly from 1.1 per 100,000 in the 1950s to 0.08 per 100,000 in the 1960s. While it should be noted that this coincided with a period of lower typhoon activity as well, when activity increased again in the 1990s the lower mortality rates persisted. The number of deaths due to flooding also showed a notable improvement with a 66% reduction in mortality from 1950s to 1960s and a further 58% decrease in the next decade7 though no significant variation in precipitation was observed.

On the ground

Japan is an excellent example of a nation which has successfully implemented a disaster risk reduction campaign at a national level. The great Ise Bay typhoon of 1959 caused more than 5,000 casualties and prompted the Disaster Countermeasures Basic Act of 1962 to facilitate a comprehensive and systematic administration of disaster management.8 The act covers every stage of the process: disaster prevention, emergency response to a disaster when it occurs, and recovery and reconstruction following an event. The plans included forecasting systems, defences, building codes and the preparation of evacuation routes and emergency communications. To facilitate planning the board of inquiry studied historical events, but they also considered the nature of possible earthquakes in the region, estimating the magnitudes and resulting tsunami heights which could be expected. Effectively establishing their own catastrophe model, the impacts of these physical scenarios on fatalities, infrastructure and economic outcomes were also modelled. Potential events were considered across a number of perils faced by the Japanese population including typhoons and flooding.

Much larger disaster risk reduction initiatives include the Intergovernmental Coordination Group for the Indian Ocean Tsunami Warning and Mitigation System (ICG/IOTWS) and the Risky Business Project9. The ICG/IOTWS was formed in response to one of the most devastating recent natural disasters, the Boxing Day tsunami in 2004, and is tasked with researching future risks of tsunamis, including detection, warning systems and ultimately the response to an event. The Risky Business project - possibly the most recent example of the engagement of catastrophe modelling companies with disaster risk reduction programs - is the only program established specifically to investigate the effect of climate change on hazard risks. Michael Bloomberg, former Mayor of New York City, chaired the project and, although it focuses purely on the economic risk to the United States, it exemplifies how catastrophe modelling is being utilised for new challenges such as the changing frequency of heat waves, cold spells and droughts and how this is likely to impact food production in the farming states.

Such examples highlight the emerging role of catastrophe modelling in evidence-based policy-making in this field, and the growing commitment to information-sharing between governments, aid organisations and private sector companies. Natural hazards will inevitably occur; harnessing the expertise of the modelling industry may limit the number which become natural disasters.